In this first industry spotlight, I think it is important to identify the magnitude of the funeral and cemetery businesses in the United States. Many years ago, the brokerage house Goldman Sacks was running a desk that dealt only with the stocks of those owning funeral homes, cemeteries and vendors to this space and they called the space “Deathcare”. Many of us rejected this phrase, but alas, 30 years later it is still being used. I will not but you might see it that way.

There are by most estimates about 19,000 total funeral home locations in the United States. This is down from about 21,000 just a decade earlier. Some have merged with others, but most have been sold off for their real estate value. Some were liquidated by big companies and others by mom and pop owners.

The NFDA, using the statistics from National Directory of Morticians Redbook, thinks that 89% of all locations are owned by privately owned companies. However, that means that the four public companies (SCI, Carriage, Park Lawn and StoneMor) own the other 11%. So, what about the private companies that are operating companies nationwide or throughout a region such as Foundation Partners Group? They are included in the privately owned companies.

When people sell their funeral homes, our estimate is that about 25% remain within the family. About 25% are sold to individuals buying their first or only funeral home. About 25% are being sold to a regional competitor who is expanding their growth organically. About 25% of all funeral homes that are sold are sold to the national companies.

One reason for the national companies not buying more is they are much more disciplined today than ever before. They do not buy for the sake of buying. They may buy a small firm in a market they are already located in with one or more funeral firms or a cemetery. However, the public companies are not buying today like they did in the 1980’s and 1990’s.

There are about 25,000 cemeteries. About 7,500 of them are operated as for profit cemeteries (either a legal structure that is for profit or the mentality is for profit) and about 17,500 are not for profit, owned and operated by a municipality, church, military or benevolent society.

There are a small number of new funeral homes built each year. There are less new cemeteries started each year than funeral homes. The barrier of entry to a funeral home is the cost and the threat of shrinking revenue. The barrier of entry to a cemetery is the large cost and the low return on investment as a cemetery is starting out.

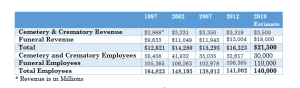

Look for more industry statistics in each newsletter! Email info@theforesigtcompanies.com to subscribe to Foresight Insights today!