One of the important steps to take when considering selling your business is to review your financial health. Part of this is to review any addbacks or adjustments to your EBITDA Figure. As this is of high importance to potential buyers of your funeral home or cemetery, we asked Jared Tanke to walk us through some examples.

Question: I am reviewing my 2023 information to prepare for a potential sale. What expenses can be added back to my financials?

Jared Tanke: When it comes to evaluating the financial health of a funeral business for potential acquisition, one key metric that buyers often consider is EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization). However, it is important to understand that EBITDA alone may not always provide a complete picture of a company’s profitability. To accurately assess the true financial performance, buyers and sellers often make certain adjustments or addbacks to the EBITDA figure. We will explore the acceptable addbacks and adjustments that buyers typically consider when evaluating an acquisition.

Non-Recurring Expenses:

Non-recurring expenses are costs that are unlikely to occur again in the future. These expenses can be adjusted or added back to EBITDA to provide a more accurate representation of the company’s ongoing profitability. In the funeral industry, examples of non-recurring expenses may include legal fees associated with a one-time litigation, costs related to a significant renovation or expansion project (i.e.: Re-bricking a retort) or expenses incurred during a rebranding initiative.

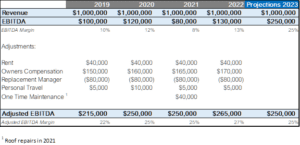

Rent paid to related entity:

It is common in the industry for independently run funeral homes to own their real estate personally or in a separate holding company, and to charge the funeral home rent. While it is ultimately ending up in the pocket of the owner, the funeral home financials will have a reduced Net Income and EBITDA. This rent expense can be added back to provide a better picture of business cash flow.

Owner’s Compensation and Perks:

In many privately-owned funeral businesses, the owners may receive compensation and perks that are above industry norms or not directly related to the day-to-day operations. When evaluating an acquisition, buyers often adjust the owner’s compensation to reflect a market-based salary for a non-owner manager. Additionally, personal expenses, or perks that are not necessary for the business operations can also be adjusted or added back to provide a clearer financial picture.

One-Time Events or Unusual Circumstances:

Occasionally, a funeral business may experience one-time events or unusual circumstances that can significantly impact its financial performance. These events could include a major natural disaster affecting operations or the physical funeral home itself. Having to repair a roof for the first time in 25 years is not something that is ordinary course of business. In such cases, adjustments are made to account for the extraordinary nature of these events and provide a more accurate representation of the business’s ongoing profitability.

As you can see in the example table above, the EBITDA of the business shows a historically low margin in the 8-13% range. However, once the adjustments have been made for rent, adjusting out owners salary and replacing them with a new manager, eliminating personal travel costs and one time maintenance, the business now reflects a true Adjusted EBITDA margin in the 22-27% range. Understanding these acceptable addbacks and adjustments is crucial when considering a sale, or just understanding the true value and profitability of your business. We would love the opportunity to represent your business for sale, walk you through the different adjustments made to EBITDA so that we can confidently approach buyers and reach a successful transition.

Do you have a question for us? Email info@theforesightcompanies.com today for a chance to have your question spotlighted in our next blog!